On December 22nd, 2017, Public Law 115-97, formally titled “An Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018” but more commonly known as the “Tax Cuts and Jobs Act,” was signed. With the signing of the Tax Cuts and Jobs Act, the United States saw the most significant, and certainly dramatic, change to the Internal Revenue Code since the Tax Reform Act of 1986. Below we highlight certain broad changes to the Internal Revenue Code, specifically tax rates or exclusion amounts, that are of particular importance and applicable to many taxpayers.

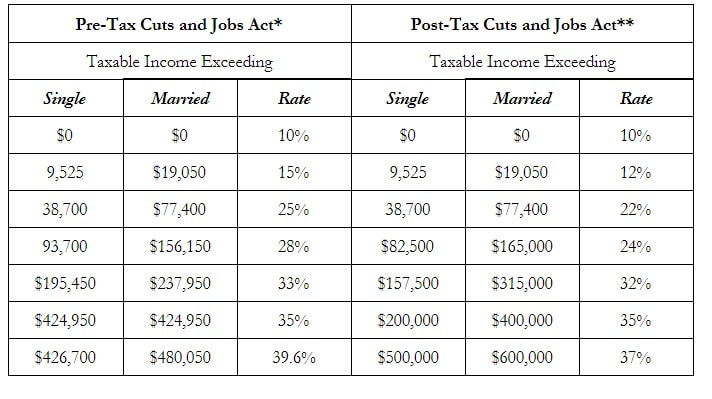

I. Individual Ordinary Income Tax Rates

I. Individual Ordinary Income Tax Rates

* Revenue Procedure 2017-58 (Oct. 19, 2017)

** All changes in individual rates are set to expire at the end of 2025

II. Pass-through Entities Tax Rate

Under the Tax Cuts and Jobs Act, there are no special tax rates or caps for taxes flowing to individuals through pass-through entities. Individual owners of pass-through entities are merely subject to the new individual ordinary income tax rates under the Act. Congress, however, did include a new 20% deduction for certain types of qualified business income (“QBI”) that is received through a pass-through entity. The Act defines QBI as the net amount of domestic qualified items of income, gain, deduction, and loss with respect to the taxpayer’s qualified trades and businesses (“QTB”). A QTB is, generally, any trade or business other than specified service businesses (e.g., professions in the fields of health, law, consulting, athletics, financial services, brokerage services, etc.).

Accordingly, an important restriction on the 20% deduction comes in the form of a cap on the amount of income eligible for the 20% deduction when an individual derives such income from their specified service businesses. This cap only allows individuals with specified service businesses to treat their income as QBI, and receive the 20% deduction, if their taxable income is less than $157,500 for single filers and $315,000 for married, joint filers. If an individual’s QBI derived from a specified service business is beyond the threshold, then the benefit of the 20% deduction for income from such specified service businesses is simply phased out over a $100,000 range, for married individuals filing jointly, and a $50,000 range for all other individuals.

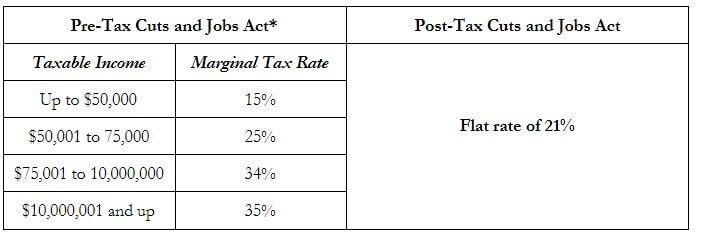

III. C Corporation Tax Rates

** All changes in individual rates are set to expire at the end of 2025

II. Pass-through Entities Tax Rate

Under the Tax Cuts and Jobs Act, there are no special tax rates or caps for taxes flowing to individuals through pass-through entities. Individual owners of pass-through entities are merely subject to the new individual ordinary income tax rates under the Act. Congress, however, did include a new 20% deduction for certain types of qualified business income (“QBI”) that is received through a pass-through entity. The Act defines QBI as the net amount of domestic qualified items of income, gain, deduction, and loss with respect to the taxpayer’s qualified trades and businesses (“QTB”). A QTB is, generally, any trade or business other than specified service businesses (e.g., professions in the fields of health, law, consulting, athletics, financial services, brokerage services, etc.).

Accordingly, an important restriction on the 20% deduction comes in the form of a cap on the amount of income eligible for the 20% deduction when an individual derives such income from their specified service businesses. This cap only allows individuals with specified service businesses to treat their income as QBI, and receive the 20% deduction, if their taxable income is less than $157,500 for single filers and $315,000 for married, joint filers. If an individual’s QBI derived from a specified service business is beyond the threshold, then the benefit of the 20% deduction for income from such specified service businesses is simply phased out over a $100,000 range, for married individuals filing jointly, and a $50,000 range for all other individuals.

III. C Corporation Tax Rates

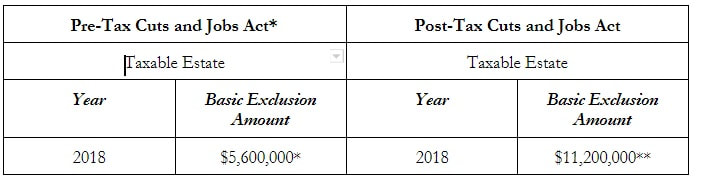

IV. Trusts and Estates Tax Rates

* Basic exclusion amount for 2018, pursuant to Revenue Procedure 2017-58, was set to be $5,600,000

** The Tax Cuts and Jobs Act doubles the basic exclusion amount under § 2010(c)(3), which will be adjusted for inflation, annually.

** The Tax Cuts and Jobs Act doubles the basic exclusion amount under § 2010(c)(3), which will be adjusted for inflation, annually.

RSS Feed

RSS Feed